SEC Commissioner Hester Peirce, the newly named head of the regulator’s crypto task force, has long been a proponent of the crypto industry as one of the Republicans overseeing the federal securities regulator. She discussed her approach with CoinDesk in late February.

You’re reading State of Crypto, a CoinDesk newsletter looking at the intersection of cryptocurrency and government. Click here to sign up for future editions.

‘Right the ship’

The narrative

SEC Commissioner Hester Peirce spoke with CoinDesk on Feb. 28, 2025, hours before U.S. President Donald Trump announced his White House crypto summit.

Why it matters

The U.S. Securities and Exchange Commission is one of the key regulators overseeing the crypto sector in the country, and has been the source of much ire. Peirce, who has served as a commissioner since 2018, is now looking to change the regulator’s approach to the entire industry. As part of this, the SEC is hosting an event on crypto policy on March 21.

Breaking it down

Just to get right into it, obviously, it’s been, I think, an eventful five weeks now, give or take, since President Donald Trump took the oath of office and resumed his presidency. The big thing in your world is the new crypto task force that you’re heading up, as far as the crypto industry is concerned. And just to begin with, I was hoping you could maybe walk through what you’ve seen and done and heard so far, and then where you expect this to go.

Yeah, let me start by giving you my standard disclaimer, which is that my views are my own views as a commissioner, not necessarily those of the SEC or my fellow commissioners. So I think it has been an exciting five weeks, and I think it was great that Chairman [Mark] Uyeda kicked off the task force, and decided to give us the ability to think about a lot of these issues in a holistic way. And so that’s exactly what we’re trying to do. I think we have been able to get a lot done already, which I’m happy about. It’s a great team, a lot of really smart people who are working very hard. And so I think the goal is to try to think about what we can just carve out and say to people, “this isn’t in our jurisdiction.” Congress, if you want to put it in our jurisdiction, that’s fine, but it’s not there.

And then with the stuff that’s in our jurisdiction, what can we do in the short term to provide some clarity or a path forward for people so that they’re not feeling that they can’t do anything out of fear that it might be within our space. So let’s provide some clear roads forward.

Those might be temporary, just bridging the gap until there’s legislation or regulation, and then trying to grapple with some of those longer term issues around tokenization of securities, around what does it look like for a broker dealer or a trading platform that’s trying to have securities alongside non-securities. Some of those more difficult issues will take some time to grapple with, and we’re trying to do all of this in a way that involves the public. We want people to be able to come in and talk to us. We want to get their suggestions for how to move forward and and and really get the best ideas and put those in place

Can you speak a bit to what you’re hearing, what kind of feedback you might have gotten already?

We’ve talked to people, and some people have started to respond. I haven’t been able to get through a lot of responses yet, but I think people are engaging seriously with what we’ve asked — the big list of questions was about 50 questions. What we’ve asked people is just respond to what [you can]. You can respond to everything if you want, but you definitely shouldn’t feel you have to respond to everything. And so I think we’re going to get some really thoughtful, very targeted responses.

Some people had already, not surprising, right? They’d already been thinking about how to move forward. So we’ve already gotten some comprehensive documents that sort of suggest how to move forward in general. And some of those are [responses] people have put out publicly. They haven’t prepared them specifically for us, but we’re looking at those kinds of things too, and we’re trying to figure out, how do we find the best ideas and and the most workable ideas and move forward with those.

Are there any areas in particular that Congress, in your view, you know, must address? Is it memecoins, is it something else, anything that the SEC, or even the SEC working with the CFTC, can’t, on their own, create a rule, or guidance for?

Well, I think they’re looking at stablecoin legislation, which I think is an area that definitely Congress has a role to play, and Congress always has a role to play, right? But I think that the market structure bills and the bills that are trying to put some clarity around what should be in our jurisdiction, what might be in the CFTC’s jurisdiction instead, could be helpful. So a lot of what is exciting about this technology is it allows for decentralization, and I think that’s what draws a lot of people to it. But as with most things, you see that people do sort of gravitate towards centralized entities. And so that would be something that I think we all need to pay attention to, because when you have centralized entities, you have the kinds of concerns that led people to want to decentralize.

You have risk of loss, risk of bad conduct by that centralized party, risk that the centralized party will treat some customers differently than others, those kinds of things. And so if you have trading platforms or other centralized intermediaries that are interacting with things that are not securities, then there is not necessarily a regulatory framework for those entities. If that’s the case, then Congress may decide that that’s something that they want to come in and write a framework for. And it seems that they do, because the bills that are out there do that. So I expect that we’ll see a lot more activity on that front this year in Congress.

Former CFTC Chair Timothy Massad said in congressional testimony, I want to say it was two or three days ago that he does not think Congress should get into market structure questions specifically. In your view, do you agree with that?

I didn’t see Chairman Massad’s commentary … I unfortunately haven’t had a chance to watch that yet, so I didn’t see his commentary. But again, I think that it’s good to have a conversation around where we need legislation and what we can do with our existing rules. He’ was chairman of the CFTC, so he has a good sense of what authority they already have.

Do you have maybe a specific timeline in mind for when the SEC could, through the work in the task force, start issuing more concrete guidance? I saw the staff statement yesterday, but anything more formal?

Well, fast is my goal. But as I said in the first statement I put out, people need to be patient too, because we want to get this. We want it. We want to do this well also. So I think we’ll just put stuff out piecemeal as it’s ready to go out, which is why you saw the memecoin statement go out. And I should emphasize that the task force is a great group of people. We’ve got really smart people there, but we are working with people across the SEC. And so you’ll see pieces coming out from different parts of the SEC. And you saw yesterday that the Division of Corporation Finance put out that statement on meme coins.

So switching tack just a little bit for a minute here, yesterday, we also saw the SEC file jointly with Coinbase to withdraw the ongoing case alleging just, I think it was a pure registrations violation claim. I know you probably can’t speak to any specific case, but could you speak a little bit to kind of the Division of Enforcement more broadly, and what we might expect, especially after the last week?

Yeah, I mean, I don’t know that I can speak to what you might expect, except to say that. And I think yesterday’s action really exemplifies this. We don’t want to use our enforcement division to write regulatory policy, and so we’re really trying to get back to using our enforcement division for its intended purpose, and letting the regulatory divisions do the hard work of figuring out how to craft rules, guidance, interpretations, and then enforcement has a rule after that, of course, to enforce the rules that are on the books. But this has just been an area where we’ve kind of gone about it backwards, and we’re trying to right the ship here.

In kind of the same vein, obviously the SEC filed to pause some of the cases against some of the companies that they’ve been litigating against. Some of those cases included fraud or related allegations. Do you expect these pauses to just kind of focus on just the pure registration/securities aspect of it, and then [they] might resume from there, or just any thoughts you might have on [that]?

We’ll assess every case on its facts and circumstances and figure out how to move forward. It’s always the goal to make sure that the policy is not being driven by the enforcement, but enforcement follows where policy is. There is certainly a role for enforcement, and there is a role for enforcement in some things related to crypto and we always have to ask the question, is there a securities violation here?

But if people are committing fraud and they’re thinking that this is a free pass to commit fraud, that’s just not the case. If we find a fraud and we don’t have authority to go after it, that’s something that we will look to find someone else who may have authority in that area, and send it their way. So I think this is really about using our resources most effectively, and that means that we can really save our enforcement resources for where there is bad conduct, as long as it’s within our jurisdiction.

So I should probably phrase this carefully, because again, I know you probably can’t speak to any specific cases, but a big one this week was against the Tron Foundation, and that case did have quite a few allegations of fraud and market manipulation. Is it possible that that’s something that you’re saying, maybe, the DOJ or another body might have kind of that greater authority, or the more relevant authority that you’re speaking of?

I can’t speak about individual cases, and we really do have to look at each case on its facts and circumstances. And there, there are a lot of cases that we have to look at. And so that’s what we’re doing.

Switching gears again. So Paul Atkins has been nominated to be the chair. Have you had a chance to speak with him about the last couple weeks?

Well, Chairman Atkins is focused, I think, on getting his hearing before the Senate and then getting confirmed. I think he’ll have plenty of time to engage with us, with the task force, with me, on these issues and others, but I’m trying to let him get through this part of the process. I know, having been through it myself, I know that it takes a lot of preparation, and there are a lot of other demands on his time right now.

Do you have any kind of expectation, just directionally speaking, what he might do with regard to crypto and some of these other issues that you’re now looking into or leading the charge on?

Well, I did work with Commissioner Atkins. I worked for him for four years, so I do know how he thinks about issues, and he definitely is someone who likes the law to be clear and then enforce. The goal is to get the law clear and then enforce it after it’s clear. So I suspect that some of the approaches that we’re taking will resonate with him and also as someone who is committed to due process, to thinking about notice and comment rulemaking, where that’s appropriate, to getting input from the people who will be affected. I think, again, some of the procedural decisions we’ve made about trying to get a lot of input from the outside, I suspect that’s something that will resonate with him. Then we’ll see when it comes down to what the individual, what does a good disclosure regime look like in this space. … Can we have some sort of safe harbor type of framework? Those are things that we’ll certainly talk with him about when he gets here.

I want to come back to the safe harbor aspect in a bit. But just one more question about Chairman Atkins. Before he was nominated, this was, I think, in February 2023, he gave an interview where he suggested that the Ripple case would be a good candidate to go up to the Supreme Court, because it could give a follow up on the Howey case. Just in your view, does that make sense? Is that something you would look forward to?

Well, again, I’m not going to speak about any particular case. The Howey Test has been around for a long time. It’s a Supreme Court case, and it is designed to interpret investment contracts, which is one element of the definition of security, and it has been applied in a lot of really different and very interesting fact patterns. By its nature, it’s going to pull in a lot of different types of things. So Howey, of course, everyone knows was about orange groves. Now it’s been applied very, very broadly in the crypto world. I think that Howey has been interpreted, maybe too broadly, and in instances, I think there are some areas of ambiguity that that the Supreme Court could address, but that I will say that is definitely above my pay grade. So if they decide to take that case, I will certainly watch that case, meaning a case related to Howey, regardless of who the parties are, I will definitely watch it closely if the Supreme Court decides to reconsider the Howey Test.

On the safe harbor front, I forget when exactly it was that you first introduced the idea of a safe harbor for the industry,

A long time ago, yeah.

Where are you now on that?

I still think we should do some kind of safe harbor. I think it would have been helpful if we had done that before. Because the sad thing about this, the way that we’ve done things, is that it’s actually disincentivized, if that’s a word, it’s discouraged people from making disclosures. And so I just want to get to a place where we actually encourage disclosure and we reward good disclosure, and I think that’s what a regime like the safe harbor regime could do. I’m not wedded to it. I think if people have better ideas, please send them in, tell us what they are. But my goal is to get to a world where people actually want to make disclosures, and they’re not fearing that if they make these disclosures, it’s going to make them a target of SEC enforcement actions. Now, of course, if you make disclosures and you lie, I mean, yes, then that’s fair enforcement game.

Do you have any kind of plans right now to either reintroduce this as a formal proposal, or just trying to get momentum back on this front?

Well, I think, as you saw from the questions that we put out, it’s definitely something we’re thinking about and want feedback on. I heard from a lot of people at the time that I put it out that they thought it would be helpful to have something like this. People didn’t love every aspect of it. I think you saw some people iterating on it. And so again, what the details are is up for debate, but it’s something that that we certainly want people to provide their thoughts on

I want to get your reaction to something that was posted online recently. Cameron Winklevoss, the co-founder of crypto exchange Gemini, posted a letter saying it was from the SEC, saying that they were going to close the investigation into that platform. But in that same post, he demanded restitution for the legal fees that they incurred, and asked for the litigators and investigators working on the case to be, I forget if it was fired or just publicly named and shamed, but I’m just curious if you have any kind of reaction to that kind of a public call.

Well, for one thing, I certainly understand. I’ve been very frustrated about how we’ve approached crypto here at the SEC over the past several years, and it has real world consequences. I get that, and it’s frustrating for me sitting here. I know it’s unbelievably more frustrating for people who are actually bearing the costs directly, and I’ve had conversations with some of those people, and it’s very difficult. But I think one thing that’s really important to underscore is that decisions about how to proceed, whether we’re going to use our enforcement tool, whether we’re going to use our rule-writing tool, are made at the commission level, and so the buck does stop at the commission. When we make bad decisions, the blame lies on us. It doesn’t lie on the staff who are directed to … They report to the chairman. They are supposed to follow the policy direction that they’re getting from the Commission. They’re supposed to execute that as effectively as they can.

We have a very good, hard working, dedicated staff at the Commission, and they seek to try to carry out the directives that they’re getting. And so I really think it’s so important for people to to understand that responsibility for decision-making, when, when the decisions are bad, when the policy direction is wrong, the blame has to lie at the commission and, and unfortunately, I think that over the past several years, we have taken an approach that has not helped the American public. It has not helped the industry to grow into being able to serve the American public as it hopes to, and it is, frankly, not serving the staff of the commission either, because it has been asking enforcement lawyers to be playing a role in writing policy. And it has been saying to policy folks, people who write rules and do interpretations and provide guidance, it said to them, you can’t do that because we’re just going to let enforcement do that. And that has led to a lot of really bad consequences. And I’m hoping we can right that ship.

Just to close out in the last few minutes, is there anything we haven’t discussed that you think people either in the crypto industry, or just the general public looking at crypto — is there anything they should keep in mind or think about over the next couple of weeks and months?

I just hope people will go to our crypto web page — it’s on the SEC website, you’ll see a link to the crypto web page. Send us a message, come meet with us. We’d love to talk to you. We’d love to hear from you, and so just stay tuned.

Awesome. Thank you very much, Commissioner, pleasure as always,

Thank you so much for having me.

Stories you may have missed

Tether’s Paolo Ardoino Says Stablecoin Issuer ‘Has Been Through Hell’, Is Cheered On at Cantor Conference: Tether CEO Paolo Ardoino is continuing his U.S. tour.

XRP Token Rises After Report That Ripple Is Close to Wrapping Up SEC Case: Ripple is one of the major SEC cases that has not yet been paused or dismissed — but reportedly, that’s coming.

U.S. SEC Acting Chair Walking Back Agency Proposal on Crypto Trading Platforms: Acting SEC Chair Mark Uyeda said in a speech that he has asked agency staff to ditch the crypto aspect of a Treasury market regulatory proposal that would have broadened the SEC’s purview to decentralized finance trading platforms.

Crypto ETFs Likely Won’t Be Approved Until New SEC Chair Is Sworn In: The SEC delayed decisions on a handful of spot crypto exchange-traded funds this week, and will likely continue to do so at least until Paul Atkins, Trump’s nominee to run the agency, is confirmed by the Senate and sworn in.

Latest Draft of U.S. Stablecoin Bill Aims to Split Power Between State and Federal Authorities: Sen. Bill Hagerty introduced an updated version of his GENIUS Act, i.e. the Senate’s stablecoin bill.

Paraguay Is Only Waiting for Crypto Law: El Salvador’s Top Crypto Regulator: Paraguay is waiting on its legislature to integrate crypto regulations, the head of El Salvador’s crypto regulator tells CoinDesk’s Tom Carreras.

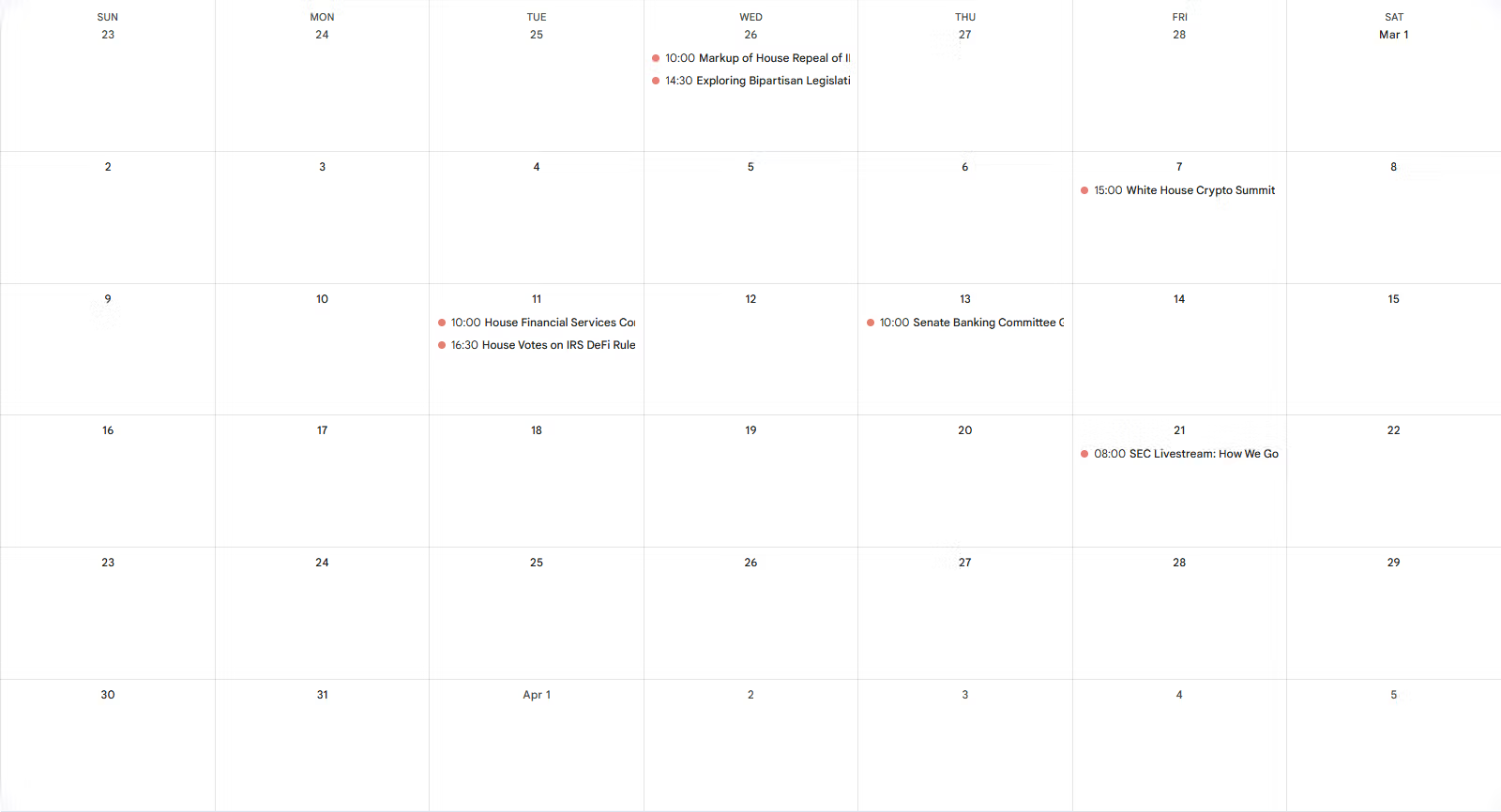

This week

Tuesday

14:00 UTC (10:00 a.m. ET) The House Financial Services Committee held a hearing on stablecoin legislation.

20:30 UTC (16:30 p.m. ET) The entire House of Representatives voted in favor of the Congressional Review Act resolution overturning the IRS’ DeFi broker rule (right after narrowly voting in favor of a continuing resolution to fund the U.S. government through Sept. 30).

Thursday

14:00 UTC (10:00 a.m. ET) The Senate Banking Committee held a markup on the Senate stablecoin bill, with a bipartisan majority of the panel ultimately voting to send the bill to the full Senate.

Elsewhere:

(Reuters) A U.S. green card holder was detained by Immigration and Customs Enforcement, apparently without a warrant or charges. Mahmoud Khalil, a Columbia University graduate student of Palestinian origin, was arrested on Saturday and faces deportation. Reuters reported that he was a negotiator between Columbia administrators and student protestors at Columbia last year, and though he reportedly attended some protests he did not occupy any academic buildings or participate in any encampments. The Department of Homeland Security and U.S. President Donald Trump both acknowledged Khalil’s detention, and a White House spokesperson told The Free Press that Khalil is not accused of breaking any laws. Presumably this case will be of interest to the free speech and civil liberty proponents within the crypto industry.

(The Wall Street Journal) People representing U.S. President Donald Trump’s family have been in talks to acquire a stake in Binance.US, and Binance founder Changpeng Zhao — CZ, who owns a majority share in Binance’s global platform — has separately been looking for a presidential pardon, the Journal reported. CZ said he had not made a deal for a pardon and has not discussed a Binance.US deal, though his statement does not appear to deny the Journal’s actual reporting. Unchained reported that CZ is trying to sell part of his stake in Binance.US, and Bloomberg reported that the talks “have included the possibility” of a World Liberty-linked stablecoin.

(The Wall Street Journal) Michelle Bowman is the frontrunner to become the new Fed Vice Chair for Supervision, the Journal reported.

(Wired) X, formerly known as Twitter, was down for a bit earlier this week, apparently due to a distributed denial of service (DDOS) attack.

(Senator Cynthia Lummis) Sen. Cynthia Lummis reintroduced a bill that would direct the U.S. government to create a Strategic Bitcoin Reserve built up by using surplus remittance fees to purchase BTC.

(ProPublica) Ernst and Young (EY) is in talks with the U.S. Department of Housing and Urban Development to trial using crypto to pay federal grants.

(Cato Institute) The Financial Crimes Enforcement Network lowered the currency transaction reporting threshold from $10,000 to $200 for transactions in 30 zip codes in California and Texas.

(The Verge) Sen. Ron Wyden, an Oregon Democrat, wrote an oped defending Section 230 of the Communications Decency Act, which protects companies from being treated as the publisher or speaker of content posted to their platforms.

If you’ve got thoughts or questions on what I should discuss next week or any other feedback you’d like to share, feel free to email me at nik@coindesk.com or find me on Bluesky @nikhileshde.bsky.social.

You can also join the group conversation on Telegram.

See ya’ll next week!